The built environment has a water problem. Buildings can be part of the solution.

A deep dive into the water findings from the 2026 U.S. Sustainable Design Report

The METROPOLIS Interface U.S. Sustainable Design Report 2026 is one of the most comprehensive looks at where the American architecture and design industry stands on sustainability today. Spanning hundreds of survey respondents, dozens of expert interviews, and a synthesis of the most significant industry research from the past two years, the report paints a candid picture: meaningful progress is being made, but structural gaps remain.

For those of us working at the intersection of buildings and water, one section of the report stands out above the rest: a frank assessment of how poorly understood, under-tracked, and under-resourced water sustainability remains compared to carbon. Here’s what the report reveals, and why the moment to close that gap is now.

The carbon-water gap is real, and growing

Ask any sustainability professional to name the carbon footprint of a building and they can reach for a methodology. Ask them the same question about water and the answer is far murkier.

While the U.S. A&D industry has built a robust body of shared knowledge around carbon (operational versus embodied emissions, lifecycle assessment, and a host of milestones tied to net-zero targets), a similar body of knowledge does not exist for water.

But, what we do know is significant. The EPA estimates that commercial and industrial buildings account for 17% of withdrawals from public water supplies. Residential buildings add another 8%. That puts total building-related operational water use at roughly 25% of public water supplies nationwide. A 2025 study published in “Resources, Conservation, and Recycling Advances” goes even further, suggesting that embodied water (the water consumed in manufacturing building materials and constructing buildings in the first place) could represent 15-18% of global freshwater use, but that number doesn’t even contain a U.S.-specific estimate yet.

Meanwhile, the demand side of the equation is getting worse. The report notes that groundwater depletion is now a “rapidly evolving crisis” in the United States. The New York Times reported record levels of water loss in 2023, and 25 of America’s largest population centers are literally sinking as the aquifers beneath them are over pumped. These aren’t abstract climate projections — they are present-tense emergencies unfolding in the same cities where construction activity is highest.

Image on the left shows a map of California subsidence and uplift. The image on the right shows total subsidence in California’s San Joaquin Valley measured by Canada’s Radarsat-2 satellite. Credit: Canadian Space Agency/NASA/JPL-Caltech

Despite all of this, there is no industry-wide water milestone or reduction target. Carbon has the AIA 2030 Commitment, with thousands of firms reporting annually and a pEUI (Predicted Energy Use Intensity) reduction methodology that’s built genuine momentum. Water has nothing comparable. Building certification systems like LEED set standards against EPA baselines and reward conservation and treatment, but they do so in isolation and without the shared framework that has made carbon reporting so effective at actually driving industry change.

Key Takeaway: Water has no industry-wide target or framework the way carbon does, despite buildings accounting for ~25% of public water use and a deepening groundwater crisis.

Data center demand is increasing

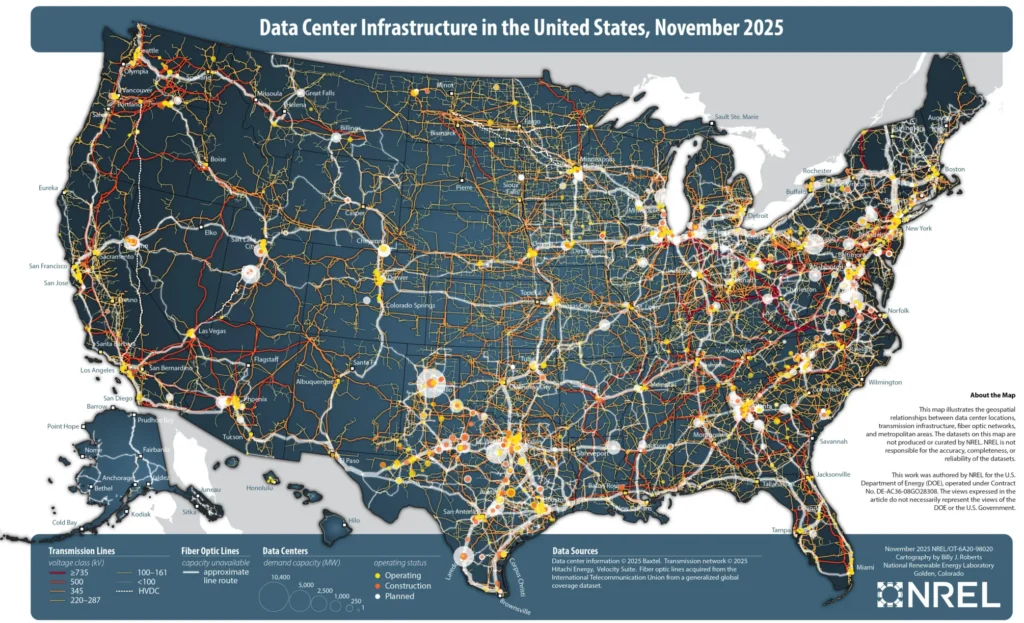

The report includes a striking data point about data centers that puts the water challenge in sharp relief. As of late 2025, the U.S. had 4,165 data centers, far outstripping any other country. These facilities used 22% more energy in 2025 than the year prior. And they’re thirsty: a single data center can consume nearly 300,000 gallons of water per day.

The report highlights a particularly difficult trade-off: water-based cooling systems are more energy efficient but increase water consumption, while air-based cooling conserves water but requires more electricity. The pressure on municipal water systems may be even greater as the data economy expands.

More than 4,000 data centers are located across the US. (Source: National Renewable Energy Laboratory)

Data centers are an extreme example, but they illustrate a broader principle. The built environment’s water demand is a moving target, and it’s moving in the wrong direction. The combination of climate-driven scarcity, aging infrastructure, population growth in arid regions, and rapidly expanding energy infrastructure is straining the centralized water systems that buildings have always relied on.

Key Takeaway: Data centers highlight the growing water crisis and they face an impossible tradeoff between water-efficient cooling (uses more energy) and energy-efficient cooling (uses more water). They’re an extreme example of a broader problem: overall demand on municipal water systems is rising fast, while supply is under increasing strain from climate change, aging infrastructure, and population growth.

The case for building-scale water recycling

The report’s “Quicker, Simpler, Easier, Better” section profiles tools and technologies that are actively reshaping how project teams approach sustainability. Water tops the list, with building-scale onsite treatment and reuse as the most compelling near-term answer to the municipal strain problem.

The logic is straightforward: if buildings are responsible for a quarter of public water demand, then buildings can be part of the solution. Onsite systems that treat and recycle water, like Epic Cleantec’s technology, can reduce demand on municipal infrastructure, insulate building owners from escalating utility costs, and create more resilient buildings that are less vulnerable to system-level disruptions.

The report notes that annual municipal water rate increases of 5–10% are common, and that this trajectory is unlikely to improve as infrastructure depletion accelerates. In Los Angeles, for example, the City Council voted in favor of more than doubling the water and sewer rates by 2028 ($5.80 → $11.96 per HCF of water used). For building owners, that’s a financial risk that onsite water reuse directly offsets.

Epic Cleantec Co-founder and CEO, Aaron Tartakovsky, in front of the treatment system at Fifteen Fifty holding treated water.

The report cites Fifteen Fifty, a luxury multifamily high rise that hosts the first approved onsite greywater recycling system in San Francisco city history, as an example of how the built environment is equipping itself and collaborating with the tech sector to achieve better results. Epic Cleantec operates and maintains this system, which recycles over 2.5 million gallons of water annually.

Key Takeaway: Buildings use 25% of public water but onsite recycling systems turn that liability into an asset, cutting municipal dependence, offsetting 5–10% annual rate hikes, and moving buildings from “less wasteful” to genuinely restorative.

Regulation is catching up

One of the persistent challenges for onsite water reuse has been regulatory. Most building and health codes were written for a centralized model of water management, and the assumptions embedded in those codes have made it difficult to permit, approve, and scale building-level systems.

That is changing. The report highlights that New York City, Los Angeles, and Austin are all actively developing or in the process of rolling out municipal mandates and financial incentives for onsite water reuse. This follows the successful implementation of San Francisco’s Article 12C which states that any new construction building over 100,000 sq ft must implement onsite water recycling. These cities represent some of the highest-density, highest-cost real estate markets in the country. Exactly the places where water strain is most acute and where the economics of water recycling are most compelling.

As of 2022, SFPUC requires all buildings over 100,000 sq ft to implement onsite water recycling.

For project teams and building owners in these markets, the implication is clear: what is currently voluntary or in regulatory gray areas is moving toward requirement in the very near future. The firms that establish onsite water programs now will have a significant advantage as these mandates come into force.

California’s SB 966 is a great example of this regulatory pathway. While the law doesn’t require any building to install a reuse system, it enables local governments to allow them. In 2025, the California State Water Board officially adopted the required regulations, which set specific treatment and pathogen-reduction standards for onsite reuse systems using greywater, roof runoff, stormwater, or certain types of other wastewater, and legacy systems are required to comply with the new standards and treatment train.

The report also notes the importance of early stakeholder alignment on sustainability goals. Water is a perfect example of where that alignment needs to happen earlier in the design process. Decisions about building size, massing, mechanical systems, and plumbing infrastructure all affect the feasibility and efficiency of onsite water reuse, and most of those decisions are locked in before sustainability consultants are typically brought to the table.

Key Takeaway: Regulations around onsite water reuse are shifting from restrictive to permissive. Firms that act now will be ahead of the curve when permissive moves to required. The catch: water reuse feasibility is determined early in design so sustainability teams need a seat at the table much sooner than is typical.

What the industry survey tells us

The report’s 2025 Sustainable Design Survey — gathering responses from over 400 professionals across every firm size and role type — reveals an industry that wants to do more on sustainability than it currently can. 48% of respondents said they’d like to incorporate “much more” sustainability into project decisions. 75% expect sustainability to continue to increase in importance over the next 5–10 years.

Page 48 of the METROPOLIS Interface U.S. Sustainable Design Report 2026

But when asked about the biggest obstacles, a familiar set of barriers emerged: client education, cost premiums for sustainable materials and systems, limited product options, and the complexity of environmental data. Water-specific knowledge gaps were evident throughout, a reflection of the broader point that water doesn’t yet have the shared language, data infrastructure, or certification momentum that carbon does.

The report’s sustainability leaders were candid about what it will take to change this. “Complexity becomes the enemy of action,” said Sean Gallagher of Diller Scofidio + Renfro. The same principle applies to water: until there are shared frameworks for measuring and reporting building water use (and shared targets for reducing it) individual project teams will continue to navigate water sustainability in isolation, without the kind of coordinated momentum that has made carbon reporting so effective.

That’s exactly the kind of infrastructure that the industry needs to build and that building owners and operators have a stake in accelerating.

Key Takeaway: The industry wants to do more on sustainability but is held back by cost, complexity, and client education gaps. Water is a particular blind spot; unlike carbon, it lacks universal measurement frameworks, reporting standards, or certification momentum, leaving teams to figure it out in isolation (or leave measuring it out all together). Until that infrastructure exists, progress will, unfortunately, remain fragmented and slow.

Looking ahead and thinking positively

The 2026 U.S. Sustainable Design Report is fundamentally optimistic. Despite political headwinds, budget pressures, and structural gaps, it documents a profession that is more serious about sustainability than it has ever been. Tools are better. Materials are cleaner. The next generation of practitioners is entering the field with deeper climate literacy and systems thinking than their predecessors.

On water specifically, the report suggests the industry is at an inflection point. The crisis is visible. The technology exists. The regulatory momentum is building. What’s needed now is the same thing that drove the carbon revolution: a shared framework, a common target, and the collective will to hold the industry accountable to it.

Buildings are not just consumers of water. They can be generators of it; treating, recycling, and returning water to use rather than sending it downstream to an already-strained system. That’s the shift the report is pointing toward, and it’s one worth building for.

The METROPOLIS Interface U.S. Sustainable Design Report 2026 was published by METROPOLIS in partnership with Interface. It synthesizes data from the AIA Firm Survey Report 2024, the AIA 2030 Commitment, the Autodesk State of Design & Make Report 2025, and numerous other industry sources. Download the report here.